QUESTION: I am looking to buy a house and have been offered a number of bonds (mortgage loans). Some have a 20-year term and others a longer one. Is there a reason I should choose the 20-year bond rather than the 30-year bond? The monthly repayments on the 30-year bond are lower, but the total amount to be repaid is higher. Which is better? Will I get penalised if I pay off my bond before the due date? ANSWER: Assuming that you are disciplined and responsible with the payment of loan obligations, choose the biggest bond (that you can get approval for in terms of your income and the valuation of the property), with the lowest interest rate and the longest payback term possible. Bond originators like Betterbond and Capcubed Home Loan Experts, who bargain on your behalf with banks and other mortgagors for the best deal, can help getting approvals. The bigger the bond, the smaller the deposit will be that you’ll have to pay. A smaller deposit means more money available for extra costs when buying property, like paying lawyers for registration and transfer cots, moving house, new insurance etc. And the lowest interest rate obviously means saving costs. A difference of only half a percentage point (0.5%) in the interest rate can, over a period of 20 years, mean a saving of more than a R100 000 on a loan for an average entry level house. The longer term will lower your monthly payback obligation and thus might enable you to get a bigger total loan approved. This is because the total bond amount approved depends, among other things, on the limited percentage of your monthly income creditors are allowed to take into account for repayment of the loan. A longer term and lower obligated monthly repayment installment also give you a bit more leeway when your income comes under pressure or you have extraordinary expenses. But a longer payback term means more total interest costs. Therefore remember this “absolute must”: Always pay back a bond as fast as possible, thereby shortening your payback term and saving huge amounts on total interest in the end. As with savings the phenomena of compound interest - or the growth of the value of money over time - can earn or cost you incredible total amounts. Bonds are normally quite flexible debt instruments with no penalties for paying back early, paying extra amounts that may become available or increasing the monthly installments. The interest is normally calculated monthly on the outstanding balance. Therefore every extra R1 paid back will save you money in the end. For example, paying back a mortgage loan in 15 years rather than over the full term of 30 years, can literally save you the price (or at least the deposit) on another house. But don’t close and deregister the bond account before the full term has expired. Keep it open as a handy available credit facility. Usually, if you’ve paid off a bond faster than the contract term, you can easily apply for a re-advance if you need money for another big purchase. The money can be available within days after your application was received. Article referenced from: https://www.fin24.com/Money/Money-Clinic/Property/money-clinic-what-kind-of-mortgage-loan-should-i-take-and-why-20190130-2

0 Comments

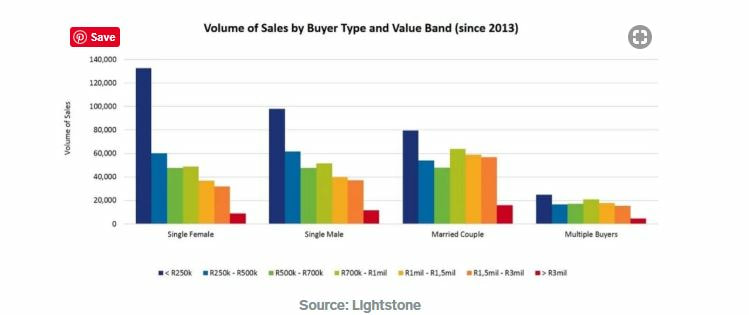

Last year, almost 72,000 single women bought residential properties in South Africa, according to the property and vehicle research group Lightstone. This is considerably more than both single men (62,000) and also more than couples - making single women the largest group of buyers in South Africa. The graph below compares the number of properties sold to single women (bright blue), to those sold to single men (dark blue), married couples (bright green) and multiple buyers (dark green).  Cindy Bezuidenhout, lead analyst at Lightstone Property, says female buyers have been steadily increasing since 2016, noticeably overtaking the male and married couple markets. Single female property buyers largely dominate in Gauteng and then by a smaller margin in the Eastern Cape. Married couples outnumber other buyer types in the Western Cape and KwaZulu-Natal. But while single women represent the most property sales, they are still buying cheaper homes. South African married couples purchase properties with the highest value, followed by single men. So far in 2019, married couples have bought properties with an average sale price of almost R1.2 million - compared to around R1 million and around R800,000 for single women. Since 2013, women have been the main buyers of houses below R250,000.  |

SO WHY US?....1. Our core values of communication and transparency means that clients are never unpleasantly surprised during the process and what you see is what you get - great results, fast and friendly Archives

February 2021

Categories |

RSS Feed

RSS Feed