The Rental Housing Tribunal exists to resolve disputes between landlords and tenants - and it’s free. The Rental Housing Tribunal is a Statutory body established in terms of Section 7 of the Rental Housing Act 50 of 1999 (as amended). It is an independent body and its members are appointed by the MEC of each province, in terms of the Rental Housing Act 50/1999, to resolve disputes between landlords and tenants regarding residential properties. An alternative to a costly court case, these tribunals have the power to summon a landlord or tenant or any other relevant party for tribunal hearing. A ruling ordering a tenant or landlord to comply with any part of the Rental Housing Act and unfair practices regulations can be issued. According to Legalwise, “if a landlord or tenant fails to comply with a ruling of the Tribunal, she/he may be convicted of an offence and sentenced to pay a fine, be imprisoned, or both. A ruling of the Tribunal is deemed to be an order of the Magistrate’s Court and may be taken on review to the High Court”. According to the Department of Human Settlements, a Rental Housing Tribunal has the authority to deal with disputes, complaints or problems between tenants and landlords in the rental housing dwellings: - Non-payment of rentals - Failure to refund the deposit - Invasion of tenant’s privacy, including family members and visitors - Unlawful seizure of tenant’s goods - Discrimination by landlord against prospective tenants - The changing of locks - Lack of maintenance and repairs - Illegal evictions - Illegal lockout or illegal disconnection of services - Damage to property - Demolition and conversion - Forced entry - House rules - Intimidation - Issuing of receipts - Municipal services - Nuisance - Overcrowding and health matters In terms of section 13(13) of the Rental Housing Act 50 of 1999, a ruling of the Tribunal is deemed to be an order of a Magistrate's Court in terms of the Magistrate's Court Act, 1994. The Rental Housing Tribunal is a free service - the government bears the costs because it is a statutory duty provision. Once a complaint is lodged, any preliminary investigation necessary will be conducted to determine whether unfair practice has taken place. The complaint may take up to 21 days to register and process, after which all relevant parties will receive a letter via post with a reference number. If the Tribunal decides that there is a relevant dispute, it may be resolved through mediation. While voluntary, this is often the best course of action. Mediation is conducted by qualified officials with many years of relevant experience, who have undergone training both internally and externally. If the dispute cannot be resolved through mediation or there is no prospect of a successful mediation, the matter will be resolved through a formal hearing. For purposes of the tribunal process, legal representation is not necessary, but it is permitted. A party can also be represented by any duly authorised person other than a legal practitioner. The hearings are usually attended by three to five tribunal members, the complainant or his/her representative(s) and the respondent or his/her representative(s). Either party can also ask other witnesses and experts to attend. Once the oath has been administered, the parties will be given an opportunity to present their cases and provide their evidence. The tribunal members will consider everything and issue a ruling. If you do not agree with the findings of the tribunal you can ask for a review before the High Court. It must be noted that the tribunals cannot order the eviction of a tenant. In such cases, the landlord will have to go to court. If the court finds unfair practices have occurred, it might refer the case back to the relevant tribunal. For more information regarding your rights as a landlord or a tenant, and contact details for Rental Housing Tribunals in your province, visit the website of the Department of Human Settlements. Article referenced from: https://www.property24.com/articles/where-can-i-turn-for-help-in-a-rental-dispute/28620

0 Comments

Where do you want to stay – in a big house with a lawn, in a small apartment?

Do you want to stay in the big city, or in a small hamlet? There are many questions to consider when deciding where and how to live, and much has nothing to do with money, as we saw in What is a financial investment? Financially the big question is, of course, “to buy or not to buy?” Is a house an investment? House prices generally go up, although some years may show much better growth than others. On average, over the long term, this growth is very close to inflation. This is to be expected. Houses are constructed from bricks and mortar and other materials, all of which become more expensive, in line with inflation, as years go by. And the wages of builders and architects, as well as the land on which a building stands, also tend to go up with inflation. A home then, which grows with inflation, but also requires some maintenance, is not a financial investment. As a rule, property is only a financial investment when it is rented out. For many people, the best strategy is this: Buy the cheapest property in which you can live comfortably. Invest the rest of your available funds in assets that actually beat inflation. Some advantages of owning your home

Some disadvantages of owning your home

Article referenced from: https://www.thesouthafrican.com/business-finance/is-buying-a-house-a-good-investment/  The Property Practitioners Act now just needs the president's signature to come into effect, and when it does it will bring about many significant changes in South Africa's property sector.

It will not only replace the Estate Agents Act, which has been in force since 1976, but will considerably broaden the scope of that legislation to cover commercial property brokers, bond originators, home inspectors, home owners’ associations, companies selling timeshare and fractional title, property developers and property managers as well as “traditional” estate agents. The new legislation also defines a managing agent as anyone who collects or receives any money payable in respect of a leased property or business undertaking or who provides, procures, facilitates, secures or otherwise obtains or markets financing for or in connection with the management of leased properties. Protection for landlords and tenants Thus everyone who sets up in business to let and manage rental properties will now fall under the provisions of the new Act as regards trust accounts and the management of client’s deposits and monthly rentals, for example, and that means better protection for both landlords and tenants. All managing agents will also need to hold a valid Fidelity Fund Certificate (FFC) in order to claim commission on any new or renewed leases. The Act also provides for a new Board of Authority to replace the current Estate Agency Affairs Board, as well as further protection for landlords, tenants and other consumers of property services in the form of a separate and independent Property Practitioners Ombud to deal with any complaints against property practitioners. The new law allows for both mediation and adjudication as part of the process for dealing with such complaints, and this should help the Ombud’s office to resolve most matters quickly and efficiently. However, it is important to note that disputes between tenants and landlords will still need to be taken before the Rental Tribunal. Other important provisions of the new legislation for landlords and tenants to note include the following:

Article referenced from: https://www.bizcommunity.com/Article/196/569/192035.html  Property professionals agree - nothing maintains your home’s value better than regular maintenance. A good home maintenance plan will safeguard against mishaps such as clogged drains, burst pipes and leaking roofs. A preventative maintenance plan will also guard against an insurer rejecting a claim due to maintenance-related faults. The condition of a property is often a deciding factor in securing a buyer, and the interior and exterior being in prime condition will make it more attractive and easier to sell. Over time, annual maintenance costs average around one percent of a property’s value. So, if your home cost R2 million you should plan to budget R20 000 a year for ongoing upkeep, repairs and special projects - from the weekly garden service to annual chimney and roof check-ups and repairs. Maintenance programme The best way to keep on top of home maintenance is to have a systematic maintenance programme, including regular weekly or monthly tasks as well as seasonal and annual jobs. The plan should cover a home’s general appearance, including manicuring the lawns and caring for plant life and repairing plumbing, electrical, heating and air conditioning problems. The basics would include:

Ideally, you should have cash available to cover emergency repairs and large occasional expenses. You could set up a separate savings or credit card account for these, and deposit funds each month so that you don’t end up paying steep credit card interest for a major repair. If you have a big expense, be sure to replenish the account for the next big-ticket job. Where possible, do the jobs yourself to save on labour costs, and hire professionals for dangerous or especially difficult jobs. Two or three pairs of hands can make the most difficult jobs much easier. Offer to help neighbours with their routine repair projects and they will return the favour when you need them. To do the hard work, you’ll need a list of reliable artisans, starting with a handyman or general contractor who can handle a broad range of jobs. Since contractors usually charge a call-out fee, wait until you have at least two or three jobs that can be done all at once. Ask around for the names of an electrician, a plumber, a carpenter and a painter. With each, start with small projects to be sure you’re satisfied with their work. Annual tasks Doors and windows – Replace broken or cracked panes of glass and apply new putty where needed. Finishes should be checked for paint deterioration and rot. Also ensure that all seals around doors and windows keep drafts out. Correct insulation around doors and windows will result in big savings on heating and cooling costs. Check that door frames are properly fitted. Bent door frames or those showing some movement during a relatively short period such as six months may indicate structural problems. Roofs – Inspect tiled roofs for damaged, loose or missing tiles which should be repaired or replaced, as a leaking roof can cause serious water damage. Check flat roofs for any blistering or bubbles. Make sure all debris is cleared from the roof and cut away any trees or branches that make contact with the roof. Chimneys – Check for loose or damaged bricks or mortar and have chimneys swept professionally once a year to remove build-up of creosote and other flammable by-products inside the chimney flue, if you burn wood. For gas-burning appliances, a licensed gas technician should be called to check that they are operating properly. Gutters – Keep gutters and downpipes clear of leaves and debris to prevent clogging. They should also be checked for blockages and leaks from holes or joints. Some sections may need to be resecured to walls or resloped to ensure they operate correctly. Remember to always make sure that water drains away from the house. Paint - adds more than just aesthetic appeal to a home - it also acts as a protective layer against the elements. Paint prevents metal areas from rusting and wooden areas from rotting. Repaint sections that have blistered or bubbled, peeled or cracked. Walls and ceilings - should be inspected for cracks in interior finishes and any damp areas. Fill any cracks and voids to allow for easy monitoring of movement between inspections. Note any water stains on the interiors and monitor regularly. Moisture or damp within walls will cause paint to bubble, and damp in the ceiling could cause sagging or even collapse. Patios and decks - Wooden decks must be properly sealed. If water is poured onto the deck and it beads the sealing is intact, but if the water is absorbed, the wood must be sanded down and resealed. All wooden sections should also be checked for rot and insect infestation. Also ensure that steps and railings are properly secured. Fixtures - Check for any leaking taps in the kitchen or bathrooms, which usually result from washers that need to be replaced. Make sure toilets are sealed and secured to the floor. Listen for toilets that run continuously. Check grouting and sealant around all bathroom fixtures and renew as necessary. The smallest amount of water seepage through the grouting can cause mould and rot behind tiles. Garages – Inspect the walls of the structure for cracks, damp and evidence of movement. Check all wooden components for evidence of rot or insect infestation and paint or treat as necessary. Driveways and pavements – Check these areas for cracks and wear, and correct hazardous uneven sections. Redirect sections that cause surface water run-off towards the house. Article referenced from: https://www.bizcommunity.com/Article/196/568/191275.html  A survey recently carried out by Lightstone has revealed a range of statistics that will be of interest to anyone keeping track of property trends in South Africa today.

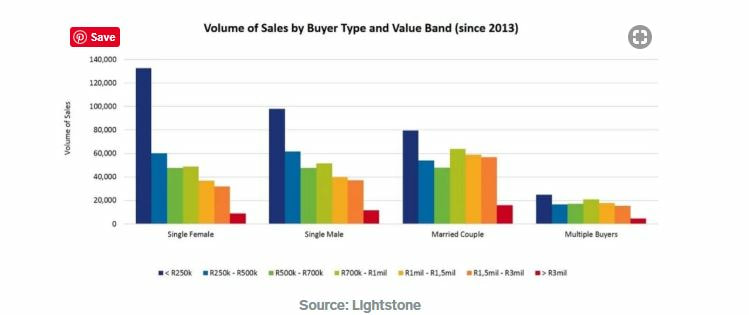

Lightstone calculated that of the 8 million registered properties in South Africa, 83% are residential. These 6.7 million homes have a combined value of R5.4 trillion, with Gauteng accounting for some R2 trillion of this figure. 67% of the total are freehold properties, 18.3% are in estates (a figure almost double that of 15 years ago) and 14.2% are sectional title units. The average value of the estate homes is roughly three times that of normal freehold properties. Gauteng remains the province with the densest residential properties as regards value and volume. Figures for SA’s municipalities show that Cape Town values are way ahead of the rest, with residential properties worth R1.6 trillion. Johannesburg comes second with R0.94 trillion and Tshwane third with R0.54 trillion. The number of homes in the Western Cape and Gauteng together is just over 50% of the total value for the country, but in value terms these two provinces account for 66% of South Africa’s homes. In Johannesburg Bryanston, Morningside and Midstream are the highest overall value suburbs, while in Cape Town Sea Point, Rondebosch and Fresnaye have captured the most value. At R19.3 million, Llandudno has the highest value per home. The far less expensive middle bracket Cape Town areas of Sillwood Heights, Hospital Hill and Voëlklip saw the highest price growth in the last year. Lightstone’s survey also reveals that single, female residential buyers in Cape Town, have increased in one year to just over 71 700 - a figure which is almost 15% higher than that of their male counterparts. The data confirm yet again that Cape Town remains a favoured precinct for property investment, with greater stability and, on average, steadier growth than other metropolitan areas. Prices here continue to be well above the average for South Africa. Article referenced from: https://www.property24.com/articles/sa-property-trends-cape-town-still-number-one-in-value/28532  QUESTION: I am looking to buy a house and have been offered a number of bonds (mortgage loans). Some have a 20-year term and others a longer one. Is there a reason I should choose the 20-year bond rather than the 30-year bond? The monthly repayments on the 30-year bond are lower, but the total amount to be repaid is higher. Which is better? Will I get penalised if I pay off my bond before the due date? ANSWER: Assuming that you are disciplined and responsible with the payment of loan obligations, choose the biggest bond (that you can get approval for in terms of your income and the valuation of the property), with the lowest interest rate and the longest payback term possible. Bond originators like Betterbond and Capcubed Home Loan Experts, who bargain on your behalf with banks and other mortgagors for the best deal, can help getting approvals. The bigger the bond, the smaller the deposit will be that you’ll have to pay. A smaller deposit means more money available for extra costs when buying property, like paying lawyers for registration and transfer cots, moving house, new insurance etc. And the lowest interest rate obviously means saving costs. A difference of only half a percentage point (0.5%) in the interest rate can, over a period of 20 years, mean a saving of more than a R100 000 on a loan for an average entry level house. The longer term will lower your monthly payback obligation and thus might enable you to get a bigger total loan approved. This is because the total bond amount approved depends, among other things, on the limited percentage of your monthly income creditors are allowed to take into account for repayment of the loan. A longer term and lower obligated monthly repayment installment also give you a bit more leeway when your income comes under pressure or you have extraordinary expenses. But a longer payback term means more total interest costs. Therefore remember this “absolute must”: Always pay back a bond as fast as possible, thereby shortening your payback term and saving huge amounts on total interest in the end. As with savings the phenomena of compound interest - or the growth of the value of money over time - can earn or cost you incredible total amounts. Bonds are normally quite flexible debt instruments with no penalties for paying back early, paying extra amounts that may become available or increasing the monthly installments. The interest is normally calculated monthly on the outstanding balance. Therefore every extra R1 paid back will save you money in the end. For example, paying back a mortgage loan in 15 years rather than over the full term of 30 years, can literally save you the price (or at least the deposit) on another house. But don’t close and deregister the bond account before the full term has expired. Keep it open as a handy available credit facility. Usually, if you’ve paid off a bond faster than the contract term, you can easily apply for a re-advance if you need money for another big purchase. The money can be available within days after your application was received. Article referenced from: https://www.fin24.com/Money/Money-Clinic/Property/money-clinic-what-kind-of-mortgage-loan-should-i-take-and-why-20190130-2 Last year, almost 72,000 single women bought residential properties in South Africa, according to the property and vehicle research group Lightstone. This is considerably more than both single men (62,000) and also more than couples - making single women the largest group of buyers in South Africa. The graph below compares the number of properties sold to single women (bright blue), to those sold to single men (dark blue), married couples (bright green) and multiple buyers (dark green).  Cindy Bezuidenhout, lead analyst at Lightstone Property, says female buyers have been steadily increasing since 2016, noticeably overtaking the male and married couple markets. Single female property buyers largely dominate in Gauteng and then by a smaller margin in the Eastern Cape. Married couples outnumber other buyer types in the Western Cape and KwaZulu-Natal. But while single women represent the most property sales, they are still buying cheaper homes. South African married couples purchase properties with the highest value, followed by single men. So far in 2019, married couples have bought properties with an average sale price of almost R1.2 million - compared to around R1 million and around R800,000 for single women. Since 2013, women have been the main buyers of houses below R250,000.   More than 50% of home loan applications need to be submitted to at least two and sometimes three or four banks before being accepted - but fortunately, home buyers no longer need to traipse around from bank to bank with files full of paperwork while crossing their fingers that they find one prepared to give them a bond at a reasonable interest rate.

These days you just need to submit your application through a reputable originator. They use an electronic multi-lender submission process which means that prospective borrowers only have to complete one application and assemble one set of supporting documents before their application is simultaneously submitted to a number of banks, including their own bank. However, bond origination is not just about convenience, their consultants also know what the different banks require and keep up with all the different home loan products they currently have on offer. This means they can direct and motivate your application to those lenders most likely to approve it, and so significantly increase your chances of obtaining a home loan. More than 75% of the applications submitted via a bond originator are approved – which is a big improvement on the general approval rate of 50% or less. Thirdly, applying through an originator immediately signals to each bank that there are other lenders competing for your home loan business, and encourages them all to immediately make their best offer as regards the interest rate and terms that would be applicable to your bond. This not only speeds up the approval process but ensures that you are getting the very best interest rate available in your particular financial circumstances. And that is critical because even a small difference in the rate can cut many thousands of rand off the total cost of your home. They can also help you work out what size bond you can afford on your current salary and assist you to obtain a pre-qualification certificate for that amount. This will enable you to focus on homes that are within your budget, signal to sellers that you are a serious buyer and give you leverage in price negotiations that could save you even more on the total cost of your home. Article referenced from: https://www.property24.com/articles/applying-for-a-home-loan-good-reasons-to-use-a-bond-originator/28411

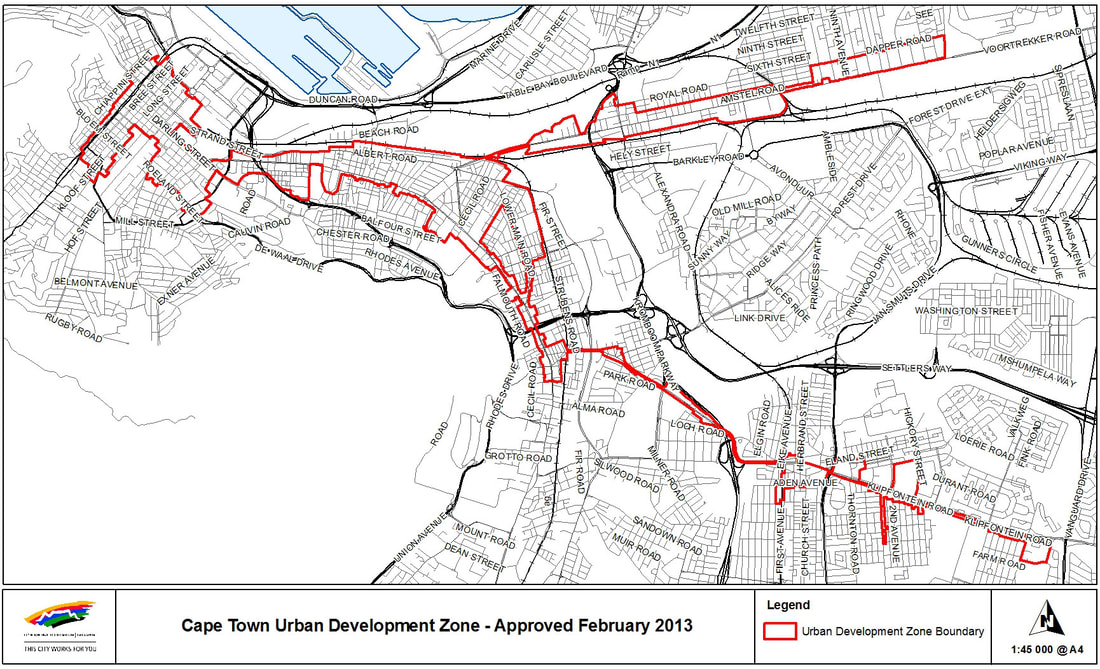

Urban Development Zone – Tax Incentive to purchase property In 2008 Cape Town Partnership began collaborating with the City of Cape Town on a shared ten-year vision and workable plan for the turnaround of Cape Town’s central city. The initiative was so successful that the area was enlarged to include Woodstock among other areas. As part of this workable plan the Urban Development Zone was set up as an income tax rebate used to incentivise property development (new builds or renovations) in these areas. The benefit to the purchaser of these developments is that as a taxpayer he can reduce his taxable income, and thus pay less tax to SARS. This depreciation type allowance allows purchasers large deductions from their taxable income and this could result in a reduction of income tax liability or a tax refund. It is in effect a Depreciation Allowance, spread over 11 years. The allowance is calculated on 55% of the purchase price, for new buildings. It is spread over 11 years. Year one – 20% of the 55% Year two to 11 – 8% of the 55% UDZ Tax Allowance Calculation Purchase Price of unit - R 1, 100 000 UDZ Allowance (55% of purchase price) - R 605 000 Year one allowance 20% - R 121 000 Year two to eleven allowance 8% yearly - R 48 400 Total allowance over 11 year period - R 605 000

SA’s land-reform programme is deemed to have failed since 1994. After a survey of title deeds, the government says blacks own 4 percent of private land, and only 8 percent of farmland has been transferred to black hands, short of a target of 30 percent that was meant to have been reached in 2014. The government is under pressure to expedite land reform. It views expropriation without compensation as a way to correct imbalances of the past, decrease inequality, encourage land ownership and agricultural sector participation by black people. An amended Expropriation Bill was passed by Parliament last year but sent back to the legislature by President Jacob Zuma because of constitutional failings. The bill effectively does away with the "willing-buyer-willing-seller" concept and reflects section 25 in the Constitution. In December 2017, the South African Parliament voted in favour of a motion to amend its Constitution to allow expropriation of land without compensation. The acceptance of the motion follows a resolution by the ANC at its 54th national elective. To do this, it urged the government to begin a process to amend Section 25 of the Constitution. This clause allows for expropriation of land with compensation. Compensation is critical as it recognises that property owners may use their property for productive purposes or may have mortgages on their property. This was then referred to the Constitutional Review Committee which will consider whether expropriation without compensation is sensible and especially how section 25 should be amended. The committee has until 31 August 2018 to report back to Parliament. The Committee will compile a white/green paper and lawmakers, attorneys and the public will then be engaged to comment on it. In order to finally pass the resolution, it must be voted in favour by at least six of the nine National Council of Provinces and two thirds (about 67%) of the National Assembly would have to agree to change Section 25. The ANC holds 62% of the seats in the National Assembly. It will have to join with other opposition parties like the EFF (holding 6.4% of seats) to amend the Constitution. Some have even argued that a 75% vote will be required as to change Section 25 of the Constitution impinges on the founding values of the Constitution. Some estimate that this process may take years as South Africa’s whole legal jurisprudence on property ownership is affected. Other pieces of legislation will also have to be amended. These include the National Credit Act and the Expropriation Act, which anticipates just and equitable compensation. The ANC is also considering reforms that would give title deeds to about 17 million people who live in the “homelands” to which most black South Africans were sent under Apartheid. Giving these people land title will maybe unlock capital, reduce poverty and create tax revenue for infrastructure development and boost GDP.  A team led by deputy public works minister Jeremy Cronin has drafted an amendment to a forthcoming expropriation law which also sets out which clearly which land will be expropriated without compensation. He states it is possible to achieve this without amending the constitution by adding a limitation into the forthcoming expropriation bill. He identifies abandoned buildings, unutilized land, commercial property held unproductively and underutilized state-owned land as possible land that can be utilized. Many have asked why this is taking place now. Most authors have speculated that its due to the national election taking place next year to alleviate the loss of votes the ANC have endured. Will this change apply to residential property and should we be worried? In his state of the nation speech, Ramaphosa said that expropriation of land without compensation must take place in a manner that does not harm the economy and improves food security. Other MP’s have indicated that the state is only targeting agricultural land. The final set of resolutions on land expropriation emphasises the need to redistribute vacant land and underutilized state owned land. If the expropriation committee decides it’s going to expropriate an entire suburb. Firstly, anything that is done cannot prejudice the banks. This is clearly shown by the way courts have dealt with evictions in the past and have recognised that mortgages have to be respected. This is because in order for an economy to function, money has to be advanced. If the government elected to expropriate properties where bonds were in place, the banks would stop granting bonds because there would be no guarantee of a return on investment. If the banks left the property market, the property market would fail. It is important to remember that homeowners have rights which are protected by the courts. The expropriation bill is clear on this. Thus, a decision by the expropriation committee may lead to the courts being swamped with cases should the government try to do away with any expropriation decision through.” Now that Zuma has been done away with, we hope that Cyril Ramaphosa will do everything possible to regain investor confidence, both domestic and international, and that he will put mechanisms in place to drive this process. If so, random expropriation of residential property would be non-sensical. The EFF Secretary-General, Godrich Gardee, and asked him about the “second Zimbabwe” notion. He stressed the world of differences between what’s happening here, and what happened across the border: “Zimbabwe’s policy wasn’t land reform, it was a land grab. What we are doing is constitutional. It requires decisions taken in Parliament. It is subject to laws, and the general application of our constitution. Everything that happens here will be legal, and follow procedure. It simply cannot be compared to Zimbabwe.”

|

SO WHY US?....1. Our core values of communication and transparency means that clients are never unpleasantly surprised during the process and what you see is what you get - great results, fast and friendly Archives

February 2021

Categories |

RSS Feed

RSS Feed