The property market has shifted notably over the last 18 months as the fall-out from the weak political and economic climate, poor growth and credit downgrades continue. Where it was a sellers’ market until early last year, there has been a progressive shift this year which has manifested in lower demand, rising stock levels combined with a decline in buyer confidence, flat price growth and deals taking longer to conclude. The outcome is that we head into 2018 with a buyer’s market for most areas. It is concerning to most agents that there is still a lag on the sellers’ side of the equation, with price expectations out of step with the market. The result, is an overall weaker market with low levels of liquidity that now favours buyers in most areas. Overall, the market is down by about 15%-20% from the 2015-highs. Yet, we operated in 2017 with slightly improved fundamentals compared to 2016, being a lower repo rate (6.75% vs 7% in 2016) and slower inflation (5.3% vs 6.5% in 2016), According to property experts, the reported slow-down in ‘semigration’ is also attributable to the slow rate of sales in other provinces combined with the high prices in the Cape – which has now also put a dampener on this market. The holiday and investment market has also slowed as an inevitable fall-out from the weak confidence levels. Finance minister Malusi Gigaba painted a subdued outlook in his mini budget, and that the country is in for a tough economy and property market in 2018. While by no means gloom and doom, it is a period of prudence ahead for property, he said. While looking forward to a busier summer period, especially the first part of the year when there is always higher activity, the biggest challenge for the economy and market remains the unstable political climate and poor economic decisions making. That said, history has shown SA property to be a good investment with growth rates that generally outpace inflation during a positive economic phase as we have seen over the last few years - property remains a good investment, especially if it is your primary home. Regardless of the state of the economy, there will always be people who need to buy or sell for a variety of reasons and there is opportunity in every market. Every economy and property market goes through cycles and it is always best to take a long-term view.

0 Comments

The hassle element is certainly one reason why so many landlords engage letting agents, but should you choose to let your property out yourself, here are some tips and pitfalls to look out for: 1. Screen your tenants properly. Don't rent to anyone before checking their affordability (payslips and three to six months’ bank statements), credit history, employment references and previous landlord references. If this is not done properly, it often results in problems later - a tenant who pays the rent late or not at all, damages a property or allows undesirable visitors might have a record of doing this repeatedly. Be sure to have a written rental application with supporting documents to get all of the prospective tenant’s information. 2. Get things in writing. Be sure to use a written lease agreement to document the important facts of your relationship with your tenants - including when and how you handle complaints and repair problems. A comprehensive lease agreement is essential as it sets the tone of the relationship between a tenant and landlord by establishing what's expected from both parties and stipulating what will happen if one party deviates from the agreement. 3. Handle the deposit paid by the tenant correctly. Establish a fair system of setting, collecting, holding, and returning security deposits. Inspect and document the condition of the rental unit before the tenant moves in so as to avoid disputes over refunding the deposit when the tenant moves out. These inspections should be done with the tenant present. 4. Make repairs to the unit timeously. Keep up to date on maintenance and repairs needed to the unit and ensure these are done when requested by the tenant. If your property is not kept in good repair there is very little chance that good tenants will want to stay on. Remember, your tenant is your customer. If you want him to pay on time, make sure that he is happy. 5. Keep accurate records. Keep a detailed account of any legal or financial transactions with your tenant, as well as formal and informal correspondence. It's important to have a paper trail of any maintenance issues you've dealt with, as well as warnings or requests you've issued, so that you can refer to them should the need arise in future. Keep copies of all emails or letters to and from your tenant, and write down the dates and details of any telephone conversations you have. 6. Important note: If a verbal negotiation regarding outstanding rental has taken place where the landlord has allowed the tenant to make payment later than the rental due date, the tenant is able to rely on the defence that an informal payment plan was entered into with the landlord. As a result, the non-paying tenant is not an illegal occupant, and a judge will not be able to grant an Eviction Order. A property is a big investment and you don’t want to end up in a situation where you lose money (either through damage or bad management) on the investment because you didn’t follow all the necessary steps to prevent this from happening. Prevention is better than cure. Handling the letting and management of your property yourself means you do not have an agent deducting money from the rental income every month. However, does it really represent a saving for you? Particularly if you are new to letting a property, it may be better to pay a qualified letting agent to handle the workload, especially as their fees are tax deductible.   South Africans held their collective breath when President Jacob Zuma fired former finance minister Pravin Gordhan and replaced him with the former minister of Home Affairs, Malusi Gigaba. The repercussions were not long in coming, and Standard and Poor’s (S&P) released a public statement that it, one of the world's largest credit rating agencies, had notified the new minister that it was downgrading the country’s sovereign credit rating to junk status just hours after his appointment. The rand also reacted immediately, going into free fall in the days after the announcement was made. Rating agency S&P's downgrade of South Africa to sub-investment status will have a negative impact on the housing market and consumers as a whole. Homeowners with high debt levels should brace themselves for interest rate increases. They will need to focus on reducing their short-term debt as soon as possible and consolidate long-term debt by increasing repayment instalments to eat into the outstanding capital debt faster. What does the downgrade mean for the country? A junk status means that it will cost more for the government to borrow money, which in turn will have a knock-on effect on the consumer. Financial institutions will need to hold more money in reserve, which will make it more difficult to obtain credit, and the credit that is granted will come at a higher cost. Needless to say, the increased cost of credit will dampen consumers’ desire to purchase large-ticket items such as property and motor vehicles. Over the last while prospective home buyers have already been subjected to interest rate hikes, drought-driven food price inflation and rising electricity tariffs. An increased cost of credit would be too much to bear for consumers who are already struggling to deal with the growing cost of living. Another downside to the downgrade is the fact that it will scare away foreign investment, as the country will be perceived as far too risky. Investors will shy away because of policy uncertainty and the government's policy regarding foreign investment in land being discouraged. The higher cost of credit will also slow the building sector as developers will struggle to get the financial backing they require to initiate further projects. If there is an upside to the downgrade, it will be for consumers who have cash: Investors with access to cash will be able to benefit from the predicted price stabilisation, and will have more negotiating power in the market.  Your burning questions answered! How will the downgrade affect the average South African homeowner? There’s little doubt that this level of uncertainty is unsettling, and it’s likely to make everybody second guess everything. But South Africans are used to a high level of ‘noise’, and clear thinkers will know that it’s too soon for anybody to know the specific implications of this rating. It’ll take three to six months for the knock-on effects to be felt. Historically, the SA Reserve Bank has utilised an inflation target band of three to six percent to assist in making interest rate decisions, and with time, we will see how inflation reacts to the increased likelihood of the cost of borrowing What steps can homeowners take to soften the blow in the short term? The downgrade will increase the cost of credit as well as that of imported goods, making them more expensive. It will also slow the economy which may impact jobs. Cut down short term debt immediately and consolidate long term debt where possible. Interest rates will increase - consumers with high debt levels will be hit the hardest. How will the downgrade affect those looking to invest in property and how could it impact on first time homeowners? We believe it will impact on first time homeowners purely because they are so reliant on finance, and if the cost of finance is going to increase, they will need to come up with larger deposits. For savvy investors whose decisions aren’t affected by heightened emotions, the state of flux in which we find ourselves can present good investment opportunities. Will the banks will tighten up on the number of bonds it grants to would-be homeowners? It will cost more for banks to hold money, so they will be more stringent with their lending criteria. The stricter lending criteria may result in fewer bonds granted. However It has always been a question of an applicant meeting the affordability criteria. Will interest rates be rising over the course of 2017? None of us has a crystal ball, but should inflation rise due to the increased cost of raising finance, then it would be prudent to expect a chance of rate increases. It would be fair to say that a large number of South Africans are panicking over the recent developments – here is some reassurance: People will always need to buy and sell regardless of the economy. There are always people scaling up, scaling down, people with specific needs, etc. A marginal mitigating factor is that to some degree financial institutions have already made provision and priced in the effects that a downgrade would have on credit costs. Because of this the effect, won't be as radical as some make it out to be but a savvy homeowner would be well advised to reduce their debt levels. In conclusion The ratings downgrade does not sound the immediate end for the property market. The downgrade has in many ways already been priced into the current trading markets We therefore expect the property market to remain stable for the time being and there is no need to panic, as it is “not all doom and gloom”. We expect business as usual for the property market for now however South African consumers need to prepare themselves financially by reducing debt levels and putting away savings.

The country is experiencing the modern-day equivalent of the Groot Trek, but this time in reverse. And like the first one, which lasted from 1834-1838, the current one is also having a major effect on the country’s demographics, property and jobs market. The Groot Trek, for those who slept their way through history at school, is a term for the mass movement of mainly Dutch-speaking inhabitants who felt strongly enough about British rule over the Cape colony, that they packed their earthly goods, which included wives, children and recently-freed slaves and headed into the northern wilderness in search of land over which they could establish control and destiny. The first Groot Trek took these hardy Boers into the areas of the Free State, Northern Cape, Natal, Transvaal and even parts of Bechuanaland, which today forms part of Botswana, where they lived relatively peacefully, with only intermittent clashes with some of the indigenous people who were making their way down from upper Africa. But the Groot Trek was nothing like the Calvinistic-crusade as our history books and the murals on the Voortrekker Monument portray. While many were certainly driven by religious imperatives, a lot of them were very naughty and free-spirited, as portrayed by Robin Binckes and his controversial book Canvass Under the Sky (2012). Much of early trade with the indigenous people, says Binckes, was for dagga and even female entertainment. Discovery of diamonds Indirectly, the Groot Trek led to the discovery of diamonds in the Kimberley area in 1867. And soon thereafter, gold at the Witwatersrand in 1881, which kick-started the mining and industrial revolution that was responsible for most of the economic expansion of the 20thcentury. Admittedly, I am skipping out historical facts for which I could be attacked, but I am simply trying to make a point. For most of the 20th century, the great wealth in South Africa was created on the back of the mining boom. If you wanted to become rich in SA during this time, you headed to the golden dumps of Johannesburg to make your fortune in mining, mining finance and the service industry which served this large and booming industry. In 1970, for instance, South Africa was the top producer of gold in the world, producing more than 1 000 tons. Those days also saw the expansion of Cape-based businesses into the thriving mining and commercial headquarters of the country, with Naspers, for instance opening the Beeld newspaper in 1974 to compete with the once-mighty Perskor. Salaries and wages, and property prices were always lower or cheaper in the Cape than in Johannesburg. Cape Town wasn’t called Slaapstad for nothing. Hell, which city elsewhere in the country, nay the world, would build a super-highway which simply ends in the middle of the city unfinished to this day? Or a city that would allow someone to build the three ugliest buildings ever – the so-called tampon towers – right in front of one of the most recognisable natural heritage sites the world has to offer, Table Mountain? Stellenbosch, on the other hand, was a university town renowned for its wine estates, fruit and the rugby players it produced under the coaching skills of legendary Danie Craven. But it did, throughout this period, produce a business giant in the form of Anton Rupert, who built Remgro and thereafter Richemont into world-class business enterprises. That was then and this is now. How things have changed. In less than 20 years, the wheels of fortune have turned, and turned some more. What started out as a steady trickle from about the year 2000 of people from Gauteng and other parts of the country moving down south, mostly to retire, has now turned into a full-blown raging torrent of well-to-do and skilled people moving to the Cape in general and the Western Cape in particular. This movement gained further impetus when the Democratic Alliance took over the political management of first Cape Town itself and later the whole of the province in 2009. It is indisputable that in this period the municipalities of the Western Cape have been better and more skillfully managed with less corruption and wastage, than towns and cities in other parts of the country. The other day I went onto the website of the Drakenstein municipality (Paarl) to enquire about registering a car in my name. There was an option to send an e-mail if you had more queries, which I did (and I included my cell number). I nearly fell off my chair when I received a phone call the same day from a very friendly official asking if everything had been sorted! Imagine that happening in the great metropolis of Johannesburg where its centralised bureaucracy has become the modern-equivalent of root canal treatment without any anesthetics. The rich South and poor North The time has long gone where people mainly retired and then moved to the Cape. Now an ever-increasing number of young families with school-going children are moving down to Stellenbosch, Paarl, Somerset West and Cape Town itself. There are all kinds of numbers being thrown around. I heard from someone (who heard from someone) that about 45 000 families settled in the formal areas of the Western Cape last year. Where these numbers come from, I don’t know – but there is certainly some merit in them. And then there is the rumoured study that shows that within the next ten years, about 75% of all high-net-worth white people will be living in the Western Cape. I have tried hard to get a copy of this report but have been unsuccessful thus far. Last year, Brenthurst Wealth held an investment seminar – together with Moneyweb – at the magnificent Val de Vie estate outside Paarl. More than 75% of the people present were ex-Gautengers. Val de vie, which has just merged with Pearl Valley to become probably the largest single residential development in the country (bigger than Steyn City), is experiencing a modern-day gold rush for its available land, with record sales month after month. The most expensive stands on the so-called gentleman’s estate, ranging from R8 million to R12 million, were the ones to sell the fastest. Despite sharp increases in the prices for land, and with very high building costs, most of the phases at Val de Vie are now sold out. And, as Martin Venter, chairman and founder of the estate told me, most of the heavy hitters are not foreigners but from Gauteng. The same is happening in other parts of the Western Cape, with many developments selling out almost as soon as they’re launched. A new frail care centre being built next to De Zalze estate outside Stellenbosch has a waiting list of more than 140 people. Many areas in the Western Cape come with a natural shortage of more land to develop, such as the Atlantic Seaboard. Further inland the availability of land for development is hampered by very expensive and ever-scarcer farmland, used mainly in the production of wines and in certain areas wheat. The average house price in the Western Cape is now 40% more expensive than average prices in Gauteng and other parts of the country, and the differential is getting bigger and bigger. According to latest FNB residential property survey on home prices, the other eight provinces declined in the fourth quarter of 2016, not only in real terms but also in nominal terms, while prices in the Western Cape were up by more than 10%. It is also the only province experiencing above-inflation home rental growth, according to Tenant Profile Network. Other contributing factors There are other factors too, I feel, that are contributing to this Great Rush to the South. The Internet is a major factor as more and more careers and jobs can be done via the Internet, which reduces the need to remain in one geographical area. You can live in the Western Cape and earn a living all over the world. As this trend increases, more and more people will choose their home based on other factors than simply the need to be close to an office. The decline in the rand too has boosted this trend. At R7 and below, many people still consider emigrating to other countries with their families. At R14 to the USD this option has been reduced considerably for many people. Five years ago, R50 million would have bought you just over $7.1 million. Today, it can only buy $3.5 million which, after paying a million or two for a suitable property to live in, does not leave much for living expenses. So, what are the alternatives? Semi-grating to the Cape, away from ANC-controlled and collapsing municipalities. I speak to many other Gautengers who would like to move to the Cape, but when they realise the huge price differential between what they have now, and what they could get in the Cape, they shelve the idea. Others, however, bite the bullet and accept a reduction in home sizes as a price to pay to end up in the Cape. How long can/will this trend continue? This is difficult to say and at some stage, the trend will slow down, purely for statistical reasons. But I think this trend has some legs before it starts tapering off as those who could have moved have already done so. That’s why the Western Cape residential property market remains the only bright spot for local investors in what is a very gloomy rest of the country.

SECTIONAL TITLE SCHEME ACT and COMMUNITY SCHEMES OMBUD SERVICE 1. PURPOSE OF THE SECTIONAL TITLES SCHEME MANAGEMENT ACT 1.1 The STA now deals exclusively with the conveyancing side of sectional schemes – i.e. registration of schemes; subdivision of units; extensions of schemes etc. 1.2 The STSMA: 1.2.1 Deals exclusively with the management of Sectional Title Schemes 1.2.2 Creates an office for a Sectional Scheme Ombudsman 1.2.3 Allows disputes to be determined by the Ombudsman instead of through Arbitration 1.2.4 Allows BC’s to recover arrear levies (both special and ordinary) via the Ombudsman instead of Court action 1.2.5 Allows a BC to recover ordinary and special levies pro rata from a new owner – in the past the person who was the registered owner of a unit at the time a special levy was imposed was liable END OF STORY 1.2.6 Special/Unanimous resolutions which affect owners’ rights adversely: 1.2.6.1 If any owner feels that his/her rights are adversely affected due to a special resolution dealing with levies, his/her prior written consent must be obtained first. 1.2.6.2 The Act does not state what happens if the consent cannot be obtained or within how much time. One can only imagine that if such consent is not given then that is the end of it OR a dispute has to be declared and it is taken further. 1.2.6.3 Any unanimous resolution which will have an unfairly adverse effect on an owner cannot be implemented unless that member consents to the decision within seven days from the resolution. 1.2.6.4 In THIS instance the Act states that if this results in a dispute between an owner and a BC it may be referred to the Ombud. 1.2.7 BC’s must now create a reserve fund for future maintenance and repairs whereby 25% of annual levies must remain in reserve. 1.2.8 Any changes to Management or Conduct Rules are lodged with the Ombudsman and no longer with the Registrar of Deeds. 1.3 We now also have the COMMUNITY SCHEMES OMBUD SERVICES ACT which regulates the Ombud’s functions and powers: 1.3.1.1 The Act requires every Community Scheme (which includes ST’s; HOA’s; Share Block Schemes; Housing Schemes for Retired Persons – ANY SCHEME OR ARRANGEMENT IN TERMS OF WHICH THERE IS SHARED USE OF AND RESPONSIBILITY FOR LAND) to collect a maximum of R40 per month (depends on whether and how much normal levies are payable per month) from each unit owner to help fund this office; 1.3.1.2 It will serve to (amongst other things) deal with any and all disputes between owners or tenants and an association (being the BC; trustees or managing agent – i.e. whoever is responsible for the administration of the Scheme (In the case of ST’s no more forced arbitration as per the Old Management Rule 71); 1.3.1.3 Associations may now also apply to the Ombudsman to collect arrear levies; 1.3.1.4 When disputes are referred, the Ombud will first try the route of conciliation and if that does not work THEN it will refer it to adjudication. The adjudicator will be appointed by the Ombud. 1.3.1.5 Legal representation will not be a given – it will depend on the nature of the dispute and general all parties must agree but the Adjudicator may make a final decision in this regard. 1.3 POWERS OF ADJUDICATORS 1.3.1 To decide about any financial issues/disputes (such as accuracy of levy impositions; 1.3.2 To order a TENANT to pay rental to the association directly without any set off because of a dispute between it and the landlord and that this is seen as rental which the landlord cannot then try to sue for; 1.3.3 To deal with behavioral issues / removing illegal attachments to units/common property including pesky pets, by ordering specified action to remedy a situation or the removal of pesky pets!; 1.3.4 To overrule any decisions at any meetings including those obtained by way of special or unanimous resolution of the Adjudicator feels that it unreasonably interferes with the right of an owner OR OCCUPIER; 1.3.5 To force an association to appoint a new managing agent / fire a MA / force an MA to do what it is supposed to do; 1.3.6 To grant exclusive use over common property if the association has refused; 1.3.7 Any other order proposed by the Ombud. 1.4 HOW? 1.4.1 All disputes are referred by way of prescribed application – visit http://www.csos.org.za/ 1.4.2 All disputes must be lodged within 60 days of the dispute occurring; 1.4.3 All adjudication awards have the effect of a court order and if not carried out, the complainant may take the award to court to have it registered as such by the clerk of the court; 1.4.4 Any party unhappy with an award may appeal it to the High Court within 30 days of the order and the affected person may apply to the High Court to stay the order pending the Appeal – so this is not an automatic consequence.

From dating to banking to entertainment, technology shapes every aspect of modern life. Therefore, it is unsurprising that technology has revolutionized the real estate industry—and in the race to attract buyers, sellers and agents who do not leverage the latest tech trends risk falling behind the competition. According to the National Association of Realtors, 89 percent of today’s buyers use online tools as they search for a home. Given this statistic, it is crucial that listings include high-resolution, professionally shot photos in order to pique buyers’ interest as they scroll through multiple online listings. Beyond appealing pictures, here are some ways to secure a quick and profitable home sale through the use of technology: Allow buyers to virtually explore your home through 3D tours and videos. Videos—complete with music and narration—offer an engaging way to showcase a home, while 3D tours enable buyers to “walk” through the home room to room. By essentially allowing prospective buyers to enter the home from afar, these immersive features provide a more realistic experience than photos alone. Include interactive maps on the listing. A property’s location is one of the key considerations for buyers. Some buyers desire homes in close proximity to shopping, dining, and entertainment, while others prefer quiet neighborhoods with ample space between properties. By ensuring that listings have interactive maps that highlight the features surrounding a home, buyers are able to focus on their preferred types of communities without having to arrange in-person property tours. Help buyers envision themselves living in your home through virtual staging. In order to consider making an offer on a property, most buyers must be able to picture themselves actually occupying the home and tailoring it to fit their unique styles and needs. Home staging is a popular way to facilitate this effect. In the digital age, virtual staging has emerged as an easier and far less expensive alternative to traditional staging, which requires the rental and strategic display of furniture and other decor. By contrast, professional virtual stagers skillfully alter photos of a home by superimposing more attractive furnishings, paint colors, lighting, and more, allowing buyers to see the property at its best without generating excessive costs for sellers or agents. Give buyers a birds’-eye view of your property with drone photography. While 3D tours and videos invite buyers to digitally enter your home, drone photography offers an aerial perspective. While it is a particularly useful tool for showcasing homes that are set on large lots or boast impressive views, drone photography imbues any property with an air of grandeur. If you choose this medium, be sure to tidy your property before the photo shoot, removing debris in the yard or objects on the driveway that could detract from the quality of the images. Ask your realtor about his or her social media strategy. Most realtors maintain Facebook pages, where they share photos and information on their active listings. However, social media is constantly evolving as a marketing tool, and other platforms—including Instagram, Pinterest, and Twitter—can be used to exponentially increase your home’s exposure to potential buyers. Sites like YouTube are also powerful platforms for posting videos of your home.

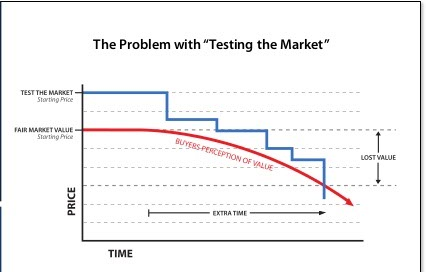

“On the one hand economists warn us that we’re likely to experience our most difficult year since 2008, with elevated inflation and currency weakness coupled with a strong likelihood of further interest rate hikes. Low GDP growth outlook, weakened consumer confidence‚ rising rates and elevated costs are set to weigh heavily on the spending and investment intentions of households and corporates,” “On the other hand, however, a number of property industry players continue to ‘talk up the market’, encouraging sellers to list their homes at higher values and persuading buyers to accept these inflated house prices as accurate reflections of the current state of a resilient property market.” He says driving this belief in rapid and consistent house price appreciation in our current economic climate is irresponsible and has many negative consequences. “Most notably, it creates disparity between seller’s expectations and buyers’ willingness to pay what sellers are asking for their properties,” says Alberts from Alexo Property Brokers “Many prospective buyers simply stall any home purchasing decision when properties appear overvalued. This creates an environment where people believe it is a good time to sell, but not to buy - and therefore homes sit on the market for longer - resulting in a ‘blockage or ‘stalemate’ situation in the marketplace, where sellers are frustrated that they can’t sell and buyers are frustrated that they cannot afford to get into the market or scale up.” What happens when buyers are ‘sitting’ is that they often begin to look at alternatives to purchasing. Alberts says this means that they look to rent rather than own, which in turn drives rental prices higher. Which is great for landlords, but not for sellers. “Not all sellers are aware how much time matters in selling a property,” says Alberts. “Sellers need to be prepared for a tightening of the market as it enters a cooldown phase. Both buyers and sellers can still realise real value in property, but should exercise caution in terms of reading into some of the overly confident public statements,” says Alberts. “There is an ideal timeframe in which to sell a property, and it falls within the first few weeks that the house is on the market. Take too long and you run the risk of creating negative perceptions about the property.” He says the number one question that every buyer asks the estate agent when becoming serious about a property is "how long has this home been on the market?". Buyers will feel that they can negotiate harder with someone whose home has been on the market for months than someone who has just recently listed. “For this reason it is imperative that sellers are honest about their situation and agree to a marketing strategy linked to a timeframe to which both seller and agency agree,” says Alberts. “There is nothing wrong with setting a high aspiration - as long as the seller’s non-urgent needs allow for a longer sales lead time, and the marketing is controlled in such a way so as not to overexpose the property.” By doing this, he says the agency can accurately represent your sentiment and urgency to buyers in an appropriate way. “Buyers want fair market value, and positioning your home at an unrealistic premium will drive off any buyers that fall into this category. Our advice to sellers is to listen carefully to what the market will bear and look at the comparable real estate sales data through the eyes of an informed buyer not an emotional seller,” says Alberts. “We believe that an appointed agency needs to fully analyse market activities and trends - whether moving upwards, plateauing, or following a downward trend - in order to best advise sellers of the correct price range that will guarantee them the best return on their investment, whilst also offering buyers market-related value. Only by providing honest, factual advice to sellers can we as property professionals ensure healthy movement within our communities.” Alberts says the fact is that, whilst over the past three years consumer confidence has shown excellent growth, it appears that the property market at large has now reached a tipping point, with the equilibrium between buyers and sellers now looking out of sync. “Buyers want fair market value, and positioning your home at an unrealistic premium will drive off any buyers that fall into this category. Our advice to sellers is to listen carefully to what the market will bear and look at the comparable real estate sales data through the eyes of an informed buyer not an emotional seller,” says Alberts. “As such, we’ve noticed a sharp rise in the number of prospective buyers who say rising prices are a barrier to buying, and instead are opting to stay put or rent until things ‘cool off’.” In terms of lending, first-time buyers are also being affected by the increase in property prices, as banks are more reluctant to take on unnecessary risk, especially when faced with the possibility of further interest rate hikes and subdued property growth in 2016. While the negative impacts of the economic slowdown have had the effect of decreasing the overall volume of property sales, Alberts says another factor to consider is the increase in transfer duty which, in conjunction with the creeping effect of capital gains tax, has especially affected the upper end of the market. He says weaker performance of residential property globally is also influencing its popularity as an asset class. Despite significantly cheaper property prices for foreign-currency buyers, there has been no major rise in home buying by foreigners, according to FNB´s Q4 2015 Estate Agent Survey, with foreign buying off its’ ‘highs’ reached around 2014. “Sellers need to be prepared for a tightening of the market as it enters a cool-down phase. Both buyers and sellers can still realise real value in property, but should exercise caution in terms of reading into some of the overly confident public statements,” says Alberts. “They should also be careful about basing their aspirations solely on property advertisements of similar properties in trying to gauge a price for their own property, as these can prove misleading.” He says the answer lies in selecting a trusted estate agent that understands current market influencers and specific area trends well enough to advise sellers of a market-related price range for their home, which takes into account their individual needs. This requires a proper analysis of what is happening in the local market and in which price bracket your property is likely to receive written interest. “In a market where buyers are highly informed and increasingly hands-on in the purchasing process, it is also vital that sellers are equally engaged, advised and enlightened,” says Alberts. Great article referenced from: http://www.property24.com/articles/are-sa-property-sellers-and-buyers-out-of-sync/23900?utm_source=newsletter&utm_medium=email&utm_campaign=agent_newsletter

CHECKING THE TITLE DEED CONDITIONS It is important, for both parties when conducting a property transaction, to check the title deed conditions before the sale agreement is signed. The purchaser will want to ensure that there are no conditions contained in the title deed which are at odds with his intentions for the property. There may, for example, be conditions restricting building or extensions on the property and /or restrictions as to how the property may be used. This is important in an age where people often look to run businesses from home. It is equally important for the seller to be aware of any such conditions, this to avoid providing any guarantees or even advice , to the purchaser in respect of the property and which runs counter to any of the title deed conditions. Where the property is bonded, the bank holding the mortgage bond will have the original title deed. A copy can be obtained from the deeds office. It is important to have a conveyancing attorney read through the deed to ensure that all conditions are identified and understood., particularly as the title deed may make reference to conditions which apply to the property, but which are contained in a previous title deed to the property. In such case that previous deed , also on file at the deeds office, will have to be located and scrutinised. Checking the title deed conditions, before entering into an agreement in respect of immovable property, is recommended to avoid any subsequent disputes between the parties, which may lead to delays in the transfer process or possibly even the cancellation of the sale. Sean de Bruin SDB ATTORNEYS COMMERCIAL & PROPERTY LAW Tel: 021 839 4441 Fax: 086 648 4053 Mobile: 082 741 1881 E-Mail: sean@sdbattorneys.co.za  |

SO WHY US?....1. Our core values of communication and transparency means that clients are never unpleasantly surprised during the process and what you see is what you get - great results, fast and friendly Archives

February 2021

Categories |

RSS Feed

RSS Feed